SLV is a complete scam, its a scalp trade set up by banks to screw over investors. Avoid it at all costs. The silver market is and has been rigged for years

SLV is a complete scam, its a scalp trade set up by banks to screw over investors. Avoid it at all costs. The silver market is and has been rigged for years

by /thehappyhawaiian - Part 1 of 2

WSB was never moving into silver. The media got the story wrong.

Think about who reads weekend financial news. Old people. The last time silver had a real short squeeze was in the 70s, and these people are now in their 70s. Who clicks on ads? Basically only old people. Dealers of gold and silver love to advertise, and media likes to make money through click-through revenue. Of course they are going to post all these stories of small unit silver selling out at dealers, they will get higher click through and sales kickbacks from the targeted ads on these articles.

If you are purchasing SLV thinking you are purchasing silver on the open market, you could not be more wrong. Purchasing SLV is the best way for an investor to shoot themselves directly in the face.

I have done some research on SLV and I have come to believe that it is essentially a vehicle for JPM and other banks to crush retail investors by manipulating the silver market.

So what are these games of manipulation that the banks have played?

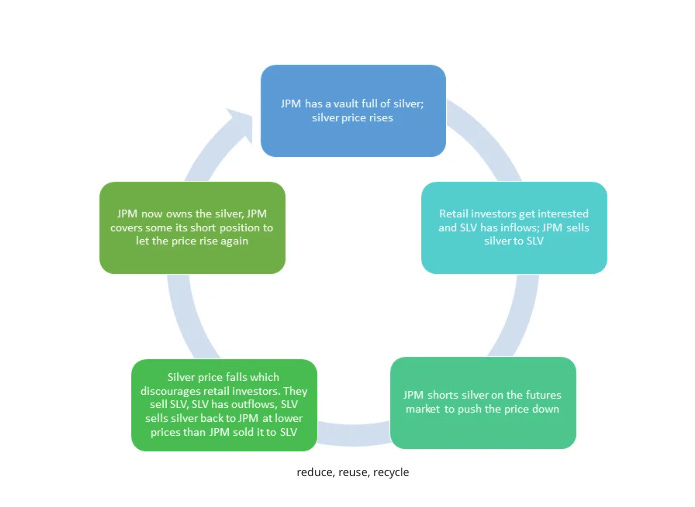

The general theme could be described as this: If banks hold the silver, the price is allowed to rise, but if you hold the silver, the price is forced to fall.

Jeff Currie from Goldman had an interview on February 4th where he dismissed the idea of a silver short squeeze, and he had one line that was especially profound,

“In terms of thinking how are you going to create a squeeze, the shorts are the ETFs, the ETFs buy the physical, they turn around and sell on the COMEX.” – Jeff Currie of Goldman

This was shocking to holders of SLV, because SLV is a long-only silver ETF. They simply buy silver as inflows occur and keep that silver in a vault. They have no price risk, if the price of silver declines, it’s the investors who lose money, not the ETF itself, so there is no need to hedge by shorting on the COMEX. Further, their prospectus prohibits them from participating in the futures market at all. So how is the ETF shorting silver?

They aren’t. The iShares SLV ETF is not shorting silver, its custodian, JP Morgan is shorting silver. This is what Jeff Currie meant when he said the shorts are the ETFs. Moreover, he said it with a tone like this fact should be plainly obvious to all of the dumb retail investors. He truly meant what he said.

What is a custodian you ask? The custodian of the ETF is the entity that actually buys, sells, and stores the silver. All iShares does is market the ETF and collect the fees. When money comes in they notify their custodian and their custodian sends them an updated list of silver bars that are allocated to the ETF.

But no real open market purchases of silver are occurring. Instead, JPM (and a few sub custodian banks) accumulated a large amount of silver, segmented it off into LBMA vaults, and simply trade back and forth with the ETFs as they receive inflows. Thus, ensuring that ETF inflows never actually impact the true open market trade of silver. When the SLV receives inflows, JPM sells silver from the segmented off vaults, and then proceeds to short silver on the futures exchange. As the price drops, silver investors become disheartened and sell their SLV, thus selling the silver back to JPM at a lower price. It’s a continuous scalp trade that nets JPM and the banks billions in profits. Here’s a diagram to help you sort it out:

An even more clear admission that SLV doesn’t impact the real silver market came on February 3rd when it changed its prospectus to state that it might not be possible to acquire additional silver in the near future. What does this even mean? Why would it not be possible to acquire additional silver? As long as the ETF is willing to pay a higher price, more silver will be available to purchase. But if the ETF doesn’t participate in the real silver market, that’s actually not the case. What SLV was admitting here, was that the silver in the JPM segmented off vaults might run out, and that they refuse to bid up the price of silver in the open market. They will not purchase additional silver to accommodate inflows, beyond what JPM will allow them to.

The real issue here is that purchasing SLV doesn’t actually impact the market price of silver one bit. The price is determined completely separately on the futures exchange. SLV doesn’t purchase futures contracts and then take delivery of silver, it just uses JPM as a custodian who allocates more silver to their vault from an existing, controlled supply. This is an extremely strange phenomenon in markets, and its unnatural.

For example, when millions of people buy GME stock, it puts a direct bid under the price of the stock, causing the price to rise.

When millions of people put money into the USO oil ETF, that fund then purchases oil futures contracts directly, which puts a bid under the price of oil.

But when millions of people buy SLV, it does nothing at all to directly impact the price of silver. The price of silver is determined separately, and SLV is completely in the position of price taker.

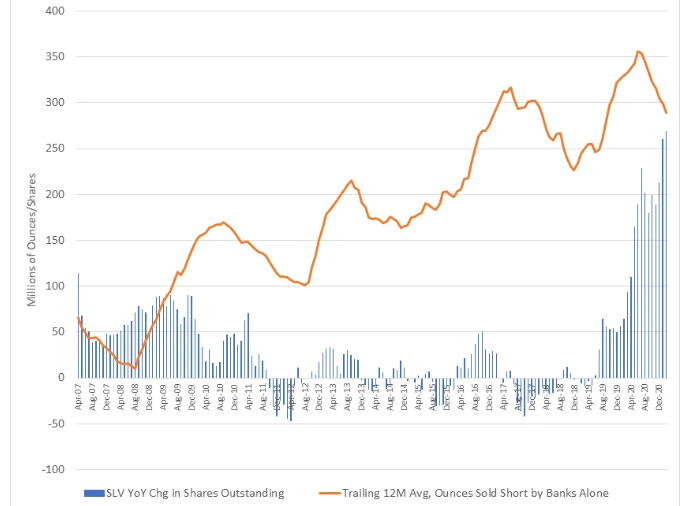

So how do we know banks like JPM are shorting on the futures market whenever SLV experiences inflows? Well luckily for us the CFTC publishes the ‘bank participation report’ which shows exactly how banks are positioned on the futures market.

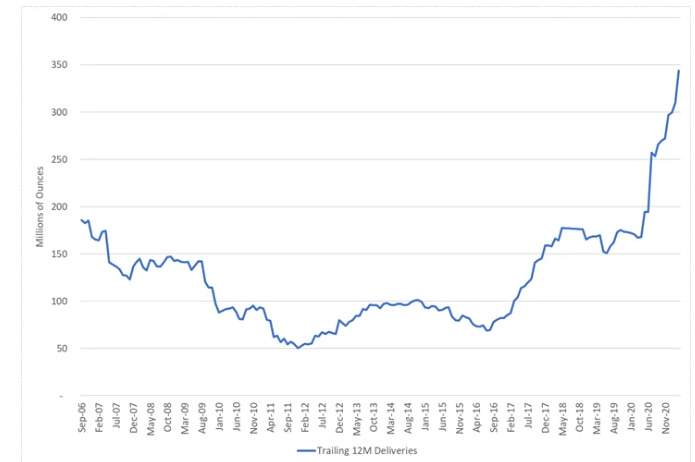

The chart below shows SLV YoY change in shares outstanding which are evidence of inflows and outflows to the ETF. The orange line is the net short position of all banks participating in the silver futures market. The series runs from April-2007 through February-2021. I use a 12M trailing avg of the banks’ net position to smooth out the awkward lumpiness caused by the fact that futures have 5 primary delivery months per year, and this causes cyclicality in the level of open interest depending on time of year.

It is evident that as SLV experiences inflows, banks add to short positions on the COMEX, and as SLV experiences outflows they reduce these short positions. What’s also evident is that the short interest of the banks has grown over time, which is also why silver is ripe for a potential short squeeze, just not by using SLV.

One other thing that is evident, is that the trend of banks shorting when SLV receives inflows, is starting to break down. Specifically, beginning in the summer of 2020, as deliveries began to surge, the net short interest among banks has actually declined as SLV has experienced inflows. It’s likely one or more banks see the risk, and the writing on the wall and is trying to exit before a potential squeeze happens (having seen what happened with GME).

For further evidence of this theme of, “If banks hold the silver, the price is allowed to rise, but if you hold the silver, the price is forced to fall” look no further than the deliveries data itself,

You’ll notice that as long as futures investors didn’t actually want the silver to be delivered, the price of silver was allowed to rise, but whenever deliveries showed an uptick, the price would begin to fall once again. This is because the shorts know that they can decrease the price of all silver in the world by shorting on the COMEX, and then secure real physical silver from primary dealers to actually make delivery. Why pay a higher price to the dealers when you can simply add to shorts on the COMEX and push the price down, and then acquire the silver you need?

But just like the graph of the bank net short position, you’ll notice that this relationship started to break down in 2020, and the price has started to rise alongside deliveries. The short squeeze is underway, and the dam is about to break.

And lest you think I’m reaching with my accusations of price manipulation by JPM, why not just listen to what the department of Justice concluded?

For JPM and the banks involved in the silver market, fines from regulators are just a cost of doing business. The only way to get banks to stop manipulating precious metals markets is to call the bluff, take delivery, and make them feel the losses of their short position.

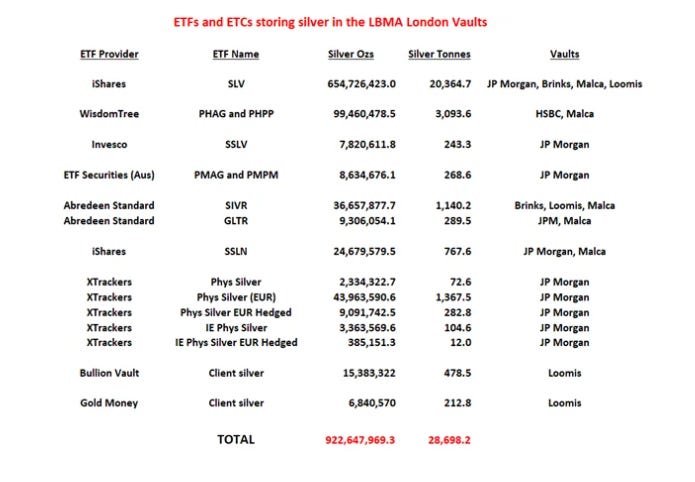

SLV is by far the largest silver ETF in the world, with 600 million ounces of silver under its control, and its custodian was labeled a criminal enterprise for manipulation of silver markets. Why should silver investors ever put their money into a silver ETF where the entity that controls the silver is actively working against them, or at a minimum is a criminal enterprise?

And let me know if you see a trend in the custodial vaults of the other popular silver ETFs:

Further exacerbating the lack of trust one should have in these ETFs, is the fact that they store the metal at the LBMA in London. Unlike the COMEX that has regular independent audits, the LBMA isn’t required to have independent audits, nor do independent audits occur. I’m not saying the silver isn’t there, but why not allow independent auditors in to provide more confidence?

So what are investors to do in a rigged game like this?

Well, there is currently one ETF that is outside this system, and which actually purchases silver on the open market as it receives inflows. That ETF is PSLV, from Sprott. Founded by Eric Sprott, a billionaire precious metals investor with a stake in nearly ever silver mine in the world, so you know his interests are aligned with the longs of the PSLV ETF (in desiring higher prices for silver via real price discovery). Further, PSLV buys its silver directly, it doesn’t have a separate entity doing the purchasing, it stores its silver at the Royal Canadian Mint rather than the LBMA, and it is independently audited. By purchasing the PSLV ETF, retail investors can actually acquire 1000oz bars and put a bid under the price of silver in the primary dealer marketplace. And if a premium occurs among primary dealers, deliveries will occur in the futures market.

This is what is starting to happen right now, a premium has developed among primary dealers, and deliveries on the COMEX have started to surge, while COMEX inventories have begun to decline. And this is happening after PSLV has added just 30 million ounces over 7 weeks (once the small contingent of silver squeezers realized SLV was a scam and started switching). Imagine what will happen if investors create 100 million ounces of demand.

Even a small portion of SLV investors switching to PSLV because they realize the custodian of SLV is a criminal enterprise, would create a massive groundswell of demand in the real physical silver market.

After the original silver squeeze posts went viral on WSB on 1/27, silver rose massively over the first 3 trading days following it. But on 1/31 a post was made about citadel being long SLV which got 74k upvotes (compared to only 15k on the original silver post). This lead to a fizzling in the momentum for the silver squeeze movement on WSB. However, given what I've explained here about how SLV is a complete scam meant to screw over investors, is it really that much of a surprise?

Additionally, that post about citadel showed them with $130m in SLV. That's only 0.04% of Citadel's AUM. Do you really think they were pushing silver because 0.04% of their AUM was in SLV? This post also didn't detail the fact that citadel also had short positions on SLV. That's what a market maker does. They have long and short positions in just about everything.

There are plenty of banks talking about a commodities super cycle, and a ‘green’ commodity super cycle where they upgrade metals like copper, but they never mention silver. Likely because banks have a massive net short position in silver.

Lets dig into the potential for a silver squeeze, starting with the silver market itself.

Silver is priced in the futures market, and its price is based on 1000oz commercial bars. A futures market allows buyers and sellers of a commodity to come to agreement on a price for a specific amount of that commodity at a specific date in the future. Most buyers in the futures market are speculators rather than entities who actually want to take delivery of the commodity. So once their contract date nears, they close out their contracts and ‘roll’ them over to a future date. Historically, only a tiny percentage of the longs take delivery, but the existence of this ability to take delivery is what gives these markets their legitimacy. If the right to take delivery didn’t exist, then the market wouldn’t be a true market for silver. Delivery is what keeps the price anchored to reality.

Industrial players and large-scale investors who want to acquire large amounts of physical silver don’t typically do it through the futures market. They instead use primary dealers who operate outside of the futures market, because taking delivery of futures is actually a massive pain in the ass. They only do it if they really have to. Deliveries only surge in the futures market when supply is so tight that silver from the primary dealers starts to be priced at a large premium to the futures price, thus incentivizing taking delivery. Despite setting the index price for the entire silver market, the futures exchange is really more of a supplier of last resort than a main player in the physical market.

Most shorts (the sellers) in the futures market also source their silver from sources outside of exchange warehouses for the occasional times they are called to deliver. The COMEX has an inventory of ‘registered’ silver that is effectively a big pile of silver that exists as a last resort source to meet delivery demand if supply ever gets very tight. But even as deliveries are made each month, you will typically see next to no movement among the registered silver because silver is still available to source from primary dealers.

So how have deliveries and registered ounces been trending recently?

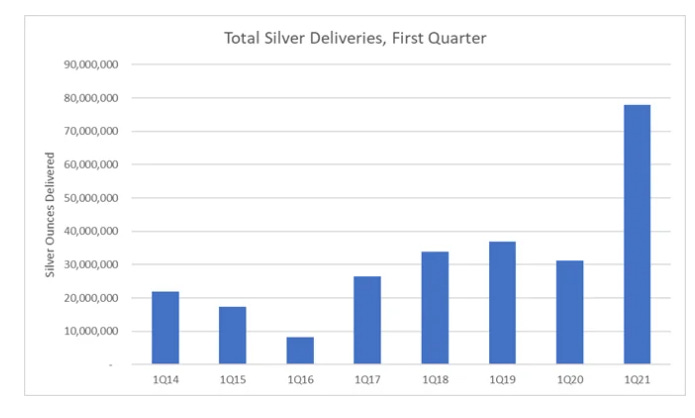

Let’s take a quick look at the first quarter deliveries in 2021 compared to the first quarter in previous years:

After adding in the 3.6 million ounces of open interest remaining in the current March contract (anyone holding this late in the month is taking delivery), 1Q 2021 would reach 78 million ounces delivered. This is a massive increase relative to previous years, and also an all-time record for Q1 from the data that I can find.

Even more stark, is the chart showing deliveries on a 12-month trailing basis (which I also showed earlier)

Note: You have to view this on an annual basis because the futures market has 5 main delivery months and 7 less active months, so using a shorter time frame would involve cutting out an unequal share of the 5 primary months depending on what time of year it is.

As you can see from the chart, starting in the month of April 2020, deliveries have gone completely parabolic. While silver doesn’t need deliveries to spike for a rally to occur, a spike in deliveries is the primary ingredient for a short squeeze. The 2001-2011 rally didn’t involve a short squeeze for example, so it ‘only’ caused silver to rise 10x. In the 2020s however, we have a fundamentals-based rally that is running headlong into a surge in deliveries that is extremely close to triggering a short squeeze.

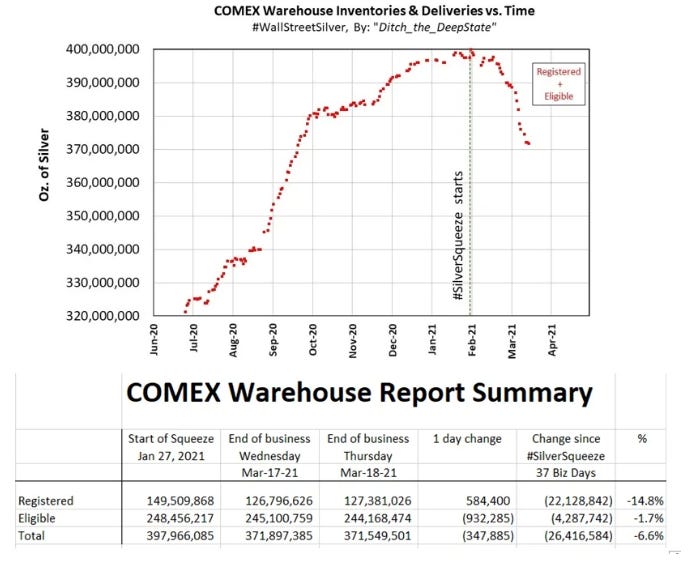

In fact this is visible when looking at the chart of inventories at the COMEX.

As you can see from the graph and the chart above, COMEX inventories are beginning to decline at a rapid pace. To explain a bit further, the ‘eligible’ category of COMEX is silver that has moved from registered status to delivered. It is called ‘eligible’ because even though the ownership of the silver has transferred to the entity who requested delivery, they haven’t taken it out of the warehouse. It is technically eligible become ‘registered’ if the owner decided to sell it. However, the fact that it is in the eligible category means that it would likely require higher silver prices for the owner to decide to sell.

The current path of silver in the futures market is that registered ounces are being delivered, they then become eligible, and entities are actually taking their eligible stocks out of COMEX warehouses and into the real physical world. This is a sign that the futures market is currently the silver supplier of last resort. And there are only 127 million ounces left in the registered category. 1/3 of an ounce, or roughly $10 worth of silver is left in the supply of last resort for every American. If just 1% of Americans purchased $1,000 worth of the PSLV ETF, it would be equivalent to 127 million ounces of silver, the entire registered inventory of the COMEX. That’s how tight this market is.

Right now we are sending most Americans a $1,400 check. If 1% of them converted it to silver through PSLV, this market could truly explode higher.

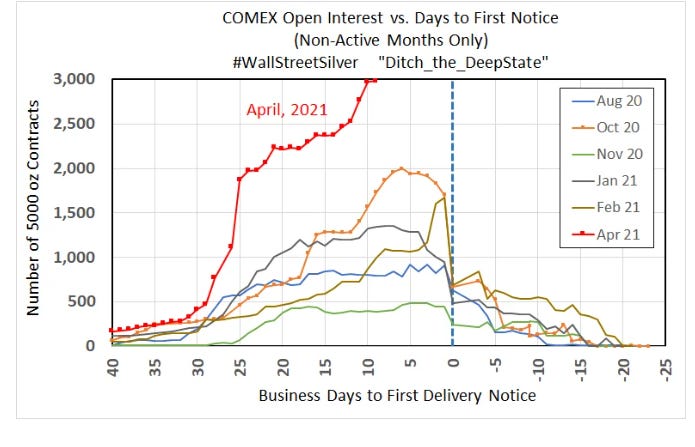

And lest you think this surge in deliveries is going to stop any time soon, just take a look at how the April contract’s open interest is trending at a record high level:

It looks almost unreal. And keep in mind the other high points in this chart were records unto themselves. That light brown line was February 2021, and look how its deliveries compared to previous years:

12 million ounces were delivered in the month of February 2021. A month that is not a primary delivery month, and which exceeded previous year’s February totals by a multiple of 4x. Open interest for February peaked at 8 million ounces, which means that an additional 4 million ounces were opened and delivered within the delivery window itself.

April’s open interest is currently at a level of 15 million ounces and rising. If it followed a similar pattern to February of intra-month deliveries being added, it could potentially see deliveries of over 20 million ounces. 20 million ounces in a non-active month would be completely unheard of and is more than most primary delivery months used to see.

Here’s what 20 million ounces delivered in April would look like compared to previous years:

So just how tenuous is the situation that the shorts have put themselves in (yes CFTC, the shorts did this to themselves)? Well let’s look at the next active delivery month of May:

end of part I